Global fintech funding reached $10.5 billion in the second quarter of 2025, marking the second consecutive quarter above $10 billion, a first since early 2023. In aggregate, fintech companies raised $21.2 billion in the first half of 2025. Deal volume fell to 804 in the second quarter, continuing the multi-year slowdown from 2021 highs. US-based

Founder Friendly Funding: The State of the Venture Markets

Based on data in Carta’s recently published State of the Markets report, the venture markets have experienced a slight uptick in number of deals and in dollars raised quarter-over-quarter. Companies on Carta’s platform completed 4% more deals and raised 12% more capital during the second quarter of 2024 compared to the first quarter. During the

Changing Trends in Private Capital

According to data aggregated by Carta, an ownership and equity management platform, private capital raising trends noticeably shifted in 2022. Companies in Carta’s database raised $107 billion in 6,123 deals in 2022. Overall, deal count declined by 29% and capital raised dropped by 50% in 2022 compared to 2021. While venture deals in 2021 broke

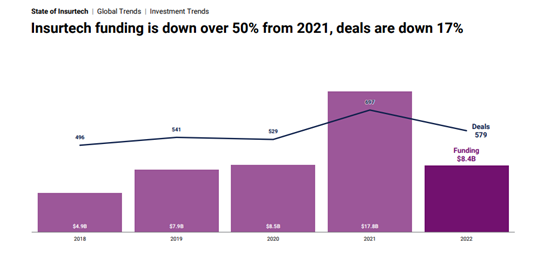

Global Insurtech Trends in 2022

CB Insights’ State of Insurtech 2022 provides a perspective on trends in the sector. In 2022, global insurtech funding fell over 50% to $8.4 billion, following 2021’s record-breaking total funding of $17.8 billion. With about $1 billion in funding, the fourth quarter of 2022 marked the lowest amount raised since the second quarter 2018.

Down

Global VC Funding Trends in 2022 Q3

The CB Insights’ State of Venture Report for the third quarter of 2022 notes that global venture funding declined to $74.5 billion in the third quarter, down 58% from the funding peak in the fourth quarter of 2021. This represents a quarter-over-quarter contraction of 34%, the largest quarterly percentage drop in a decade, with the

Unicorniphobia

In the paper, “Unicorniphobia,” Alexander I. Platt counters the viewpoint held by many legal scholars and regulators, including the SEC, that unicorns pose regulatory, financial, and social risks. Many recent articles argue that unicorns pose concerns because: they are not subject to SEC reporting and SEC scrutiny and oversight; unicorn CEOs/founders are usually innovative but

Notable Trends in the Private Markets

The private market ecosystem experienced strong growth in 2021. The number of recognized unicorns (defined as private companies having $1B+ valuation) grew from 564 in 2020 to 882 in 2021. Nasdaq Private Markets’ (“NPM”) 2021 Annual Report noted that in addition to elevated deal size for companies, secondaries have evolved as an avenue to provide

Global Venture Financing Trends in 2021 Q2

According to CB Insights’ latest State of Venture Report, global startup financing in Q2’21 reached $156.2 billion, a 157% year-over-year increase and a record quarter high. U.S. startup funding accounted for the largest portion of the global quarter total, raising $70.4 billion, followed by Asia raising $42.2 billion. Meanwhile, funding to China-based companies continued

A Look Back at Automotive & Mobility Financing Trends

Global funding for companies in the automotive and mobility sectors fell to $27.6 billion in 2020, a 5% decrease year-over-year, with 522 deals completed according to CB Insights’ recent report and webinar on the State of Mobility. While the first half of 2020 was particularly affected by the COVID-19 pandemic, the second half of

Alternative Venture Capital: The New Unicorn Investors

In a new paper, Alternative Venture Capital: The New Unicorn Investors, professor Anat Alon-Beck explores the rise of alternative venture capital (AVC) investors and the ways in which these investors are affecting unicorn companies. The paper cautions that that many of the calls being made by industry groups, such as the Institute for Portfolio