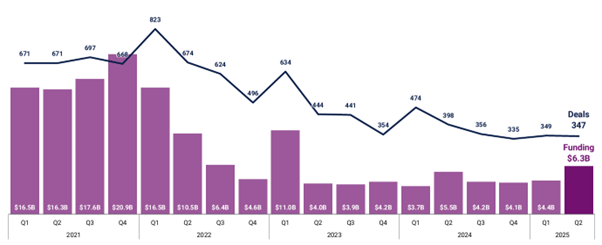

Global fintech funding reached $10.5 billion in the second quarter of 2025, marking the second consecutive quarter above $10 billion, a first since early 2023. In aggregate, fintech companies raised $21.2 billion in the first half of 2025. Deal volume fell to 804 in the second quarter, continuing the multi-year slowdown from 2021 highs. US-based fintech companies captured a record share of both deals (43%) and mega-rounds (65%), with US funding accounting for 60% of global fintech investment in Q2. In the first half of 2025, fintech companies completed 696 deals raising an aggregate of $10.7 billion.

US Quarterly Fintech Funding

Source: CBInsights State of Fintech Report Q2 2025

Late-stage deals. Investor caution persists, but late-stage companies maintained meaningful activity. Late-stage rounds represented 10% of global deal share year-to-date, with the US capturing the majority of the largest transactions. Median late-stage deal size reached $45 million, up from $30 million in 2024. Notable Q2 deals include Ramp’s $200 million Series D and Persona’s $200 million Series D, both US-based.

Mega rounds and unicorns. Mega-round activity totaled $4.2 billion in 16 deals, with the US capturing 70% of funding–including Plaid’s $575 million venture round and Rippling’s $450 million Series G. There were three new fintech unicorns in Q2 (Kalshi, Chapter, and Juniper Square) bringing the total to 325, of which 173 are US-based. Stripe remains the highest-valued fintech at $70 billion.

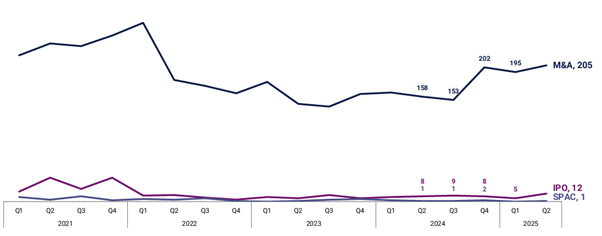

Exits. Fintech M&A volume remained elevated, with 205 transactions in Q2. Digital asset deals featured prominently, including Coinbase’s $2.9 billion acquisition of Deribit and Stripe’s acquisition of Privy. IPO activity picked up, led by Chime’s $9.8 billion debut and Circle’s $6.9 billion IPO. There was one SPAC transaction completed by Webull, valued at $7.3 billion.

Global Quarterly Fintech Exits

Source: CBInsights State of Fintech Report Q2 2025

Fintech Subsector Funding

Payments companies raised $2.9 billion in 127 deals, with the US leading at $1.3 billion. Plaid, Ramp, and Dojo topped the list, with B2B players capturing 60% of the largest payments investments. Digital lending funding reached $1.8 billion in 118 deals. The US accounted for $1.1 billion, led by Plaid’s round and Dunmor’s $150 million raise. Insurtech companies secured $1.1 billion in 89 deals. The largest were Gravie’s $144 million Series G and Bestow’s $120 million Series D financings. Wealth tech surged to $1.9 billion in funding, nearly triple the Q1 total and the sector’s strongest quarter since 2022. Addepar’s $230 million Series G and Groww’s $200 million Series F were the largest.

Read CBInsight’s full report for additional trends and data.