Funding for artificial intelligence (AI) companies totaled $47.3 billion globally in Q2 2025, the second-highest quarter on record and the third straight quarter above $40 billion according to CB Insights’ report The State of AI (Q2 2025). Total first half 2025 funding outpaced 2024 funding, raising $116.1 billion versus 2024’s $104.7 billion. Deal volume reached

Fintech Funding Trends in 2025

Global fintech funding reached $10.5 billion in the second quarter of 2025, marking the second consecutive quarter above $10 billion, a first since early 2023. In aggregate, fintech companies raised $21.2 billion in the first half of 2025. Deal volume fell to 804 in the second quarter, continuing the multi-year slowdown from 2021 highs. US-based

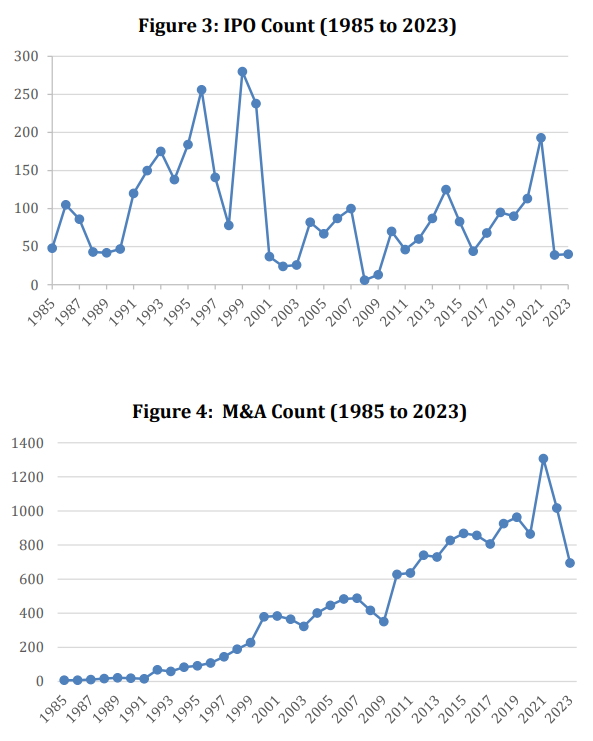

No Exit: Other Reasons to Stay Private

In No Exit, a recent paper, authors Brian J. Broughman, Matthew T. Wansley, and Samuel N. Weistein, describe how increased antitrust restrictions caused a decline in M&A exits by startups. However, instead of this leading to an increase in IPOs, companies remained private and used alternatives to access capital and liquidity.

Source: Broughman, Wansley

SEC Updates Guidance on the Use of Lock-Up Agreements in Rule 145(a) Transactions

On March 6, 2025, for the first time since 2008, the staff (the “Staff”) of the Securities and Exchange Commission updated its guidance on the use of lock-up agreements in connection with Rule 145(a) transactions (i.e., certain mergers, consolidations, reclassifications of securities and acquisitions of assets). Prior to the SEC’s update, if a person entering

Fintech Funding Trends 2024: Capital Raising Slows, Deal Sizes Grow

According to CB Insights’ State of Fintech 2024 Report (the “Report”), global fintech companies raised $33.7 billion in private placements in 2024, marking a 20% drop year-over-year. Deal volume also declined, with 3,580 offerings completed—a 17% decline from the prior year. However, this annual funding decline was the smallest in three years, signaling potential stabilization

MB Microtalk: Amendments to Beneficial Ownership Rules (13D/G)

In this MB Microtalk video, Mayer Brown’s Andrew Noreuil discusses the recent final amendments to certain beneficial ownership rules under the Exchange Act, and the impact of those changes on the reporting of beneficial ownership on Schedules 13D and 13G.

Visit our MB Microtalk page for more topics and talks.

Market Trends 2022/23: Financial Disclosures for Merger & Acquisition Transactions

This practice note discusses the main amendments to the financial disclosure requirements for acquisitions and dispositions of businesses by U.S. reporting companies, which took effect in January 2021. The amendments aim to improve the quality and relevance of the information provided to investors, reduce the complexity and costs of preparing the disclosures, and promote capital

A New Federal Exemption from Broker Registration for Qualifying M&A Brokers Became Effective on March 29, 2023 (Prior SEC No-Action Relief Has Been Withdrawn)

Although the New Federal Exemption Is Generally Aligned with the SEC’s 2014 No-Action Relief, There Are Some Notable Differences. Moreover, State Law Registration Requirements for M&A Brokers Are Not Preempted.

The U.S. Congress recently enacted a conditional exemption (the “Exemption”) from registration under Section 15(b) of the Securities Exchange Act of 1934 for qualifying brokers

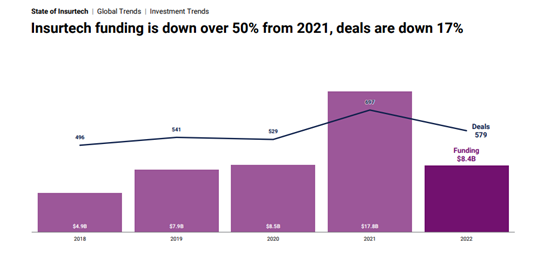

Global Insurtech Trends in 2022

CB Insights’ State of Insurtech 2022 provides a perspective on trends in the sector. In 2022, global insurtech funding fell over 50% to $8.4 billion, following 2021’s record-breaking total funding of $17.8 billion. With about $1 billion in funding, the fourth quarter of 2022 marked the lowest amount raised since the second quarter 2018.

Down

Fintech Financing Trends

Globally, the total volume of fintech deal activity, which includes financings by private companies, IPOs, and M&A activity, has declined for three consecutive quarters. Activity in the second quarter of 2022 was down 67% from the peak, which was recorded in the third quarter of 2021. Financings by private companies in the sector were at