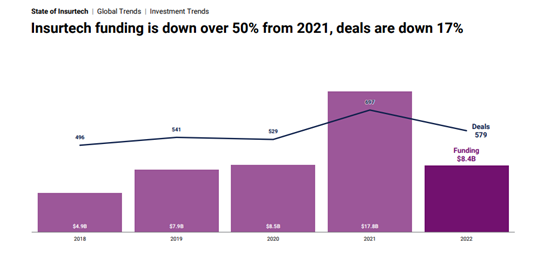

CB Insights’ State of Insurtech 2022 provides a perspective on trends in the sector. In 2022, global insurtech funding fell over 50% to $8.4 billion, following 2021’s record-breaking total funding of $17.8 billion. With about $1 billion in funding, the fourth quarter of 2022 marked the lowest amount raised since the second quarter 2018.

Down 17% from 2021, the number of deals in 2022 declined to 579 deals. The average and median deal sizes declined from their 2021 highs, returning to 2020 levels. The average deal size fell to $17.7 million in 2022, from $30.4 million in 2021. Overall, the United States led in funding and deals, followed by Europe and Asia. However, U.S. insurtech funding was down 60%. Early-stage deals accounted for the largest percentage of deals, both in the United States and globally. Early-stage deals accounted for 65% of insurtech deals globally in 2022, the highest share since 2019. The United States led in early-stage deal share, while Asia led in mid-stage deal share. In the fourth quarter 2022, Europe experienced its largest quarterly deal share since the second quarter 2019, and was the only region to see median deal size growth in 2022.

The number of M&A exits increased 40% year over year as companies capitalized on lower valuations to make acquisitions; there were a total of 81 M&A deals in 2022. Global mega round funding fell to its lowest level since 2018. Mega round funding dropped 90% in the fourth quarter 2022, with only one deal, which took place in the United States, raising $153 million. In the fourth quarter of 2022, there was only one unicorn birth, bringing the total of insurtech unicorns to 44. In the unicorn count, the United States leads the way with 25, followed by nine in Asia, eight in Europe, and one each in Australia and Latin America. In the fourth quarter 2022 there was a 67% decline in funding – marking the first quarter since the first quarter 2020 where P&C funding did not exceed $1 billion. Life and Health (L&H) insurtech fared better but still saw significant funding declines. Funding in this sector fell 58%, and deals fell 8% in 2022. Early-stage deal funding grew slightly and represented the largest L&H insurtech deal share.