According to CB Insights’ State of Fintech 2024 Report (the “Report”), global fintech companies raised $33.7 billion in private placements in 2024, marking a 20% drop year-over-year. Deal volume also declined, with 3,580 offerings completed—a 17% decline from the prior year. However, this annual funding decline was the smallest in three years, signaling potential stabilization in the fintech sector.

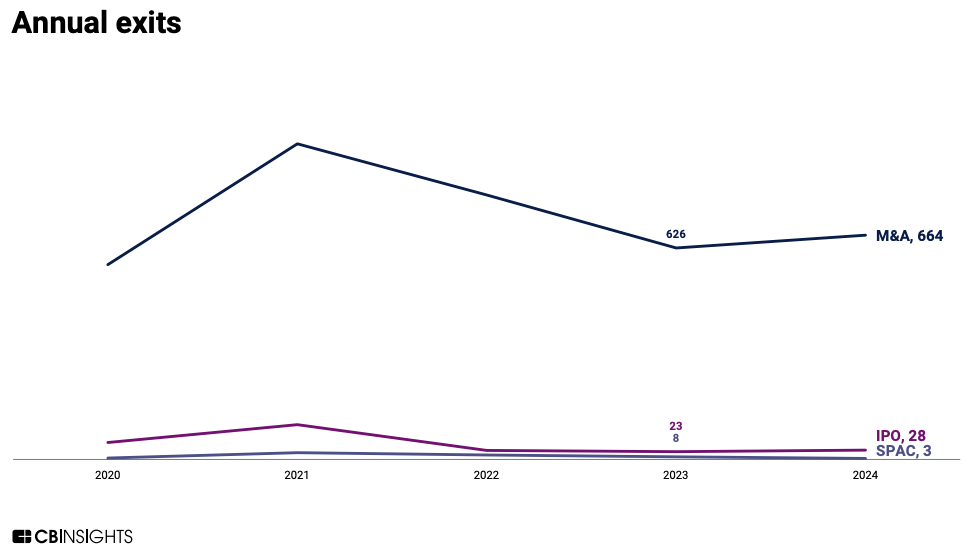

Interestingly, despite the overall funding decline, the median deal size for fintech companies rose by 33% to $4 million. Investors concentrated their capital on fewer, higher-value opportunities. Mega-rounds—funding rounds exceeding $100 million—remained a significant driver of capital, with 73 such rounds raising a total of $12 billion. Additionally, 14 new fintech unicorns emerged globally in 2024, bringing the total number of companies valued at over $1 billion to 326. The Report also highlighted an active year for M&A. A total of 664 M&A exits were completed in 2024, a 6% year-over-year increase. In contrast, IPO activity remained subdued, with only 28 IPOs completed and three fintech companies executing de-SPAC transactions.

Despite this decline in funding levels, median deal size for fintech companies increased by 33% to $4 million. Fintech companies completed 73 mega-rounds, raising $12 billion through rounds that raised over $100 million. Globally, there were 14 fintech unicorn “births”, bringing the total number of fintech companies valued at over $1 billion to 326. The Report notes that there were a total of 664 M&A exits in 2024, a 6% jump year-over-year. IPO activity remained relatively tame, with 28 IPOs completed, while only three fintech companies completed a de-SPAC transaction.

Spotlight on Fintech Subsectors

Within the fintech sector, payment solutions dominated in late 2024. Half of the top 10 equity deals in 2024Q4 were undertaken by companies innovating in mobile payment apps, cross-border payment tools, and platforms digitizing B2B payments. Banking tech gained increased investor attention as a stable subsector amidst regulatory uncertainty. In 2024, 38% of all banking tech deals were mid- or late-stage. While mid- and late-stage deals rose by 4 percent year-over-year across the broader fintech sector, banking tech saw a larger increase of 17 percent. Investors appeared to favor established solutions in a time of market volatility and evolving regulation. As fintech adapts to shifting investor priorities and regulatory landscapes, the sector’s focus on scalable, proven solutions suggests continued evolution and resilience in 2025.