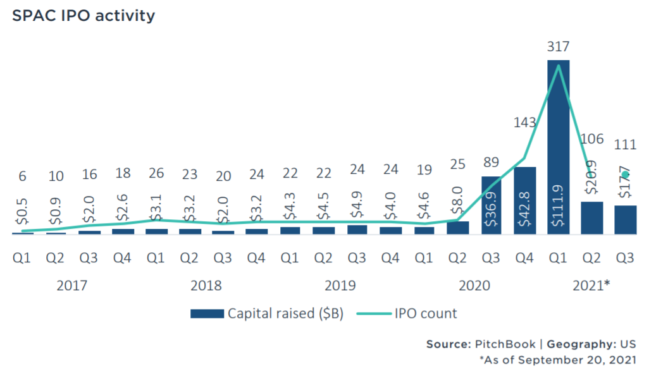

In a report issued by Pitchbook related to the SPAC market, quarterly trends show a recent dip. There were 317 SPAC IPOs completed in the first quarter of 2021, but a steep decline in the second quarter, with only 106 SPAC IPOs completed. Consistent with this trend, the third quarter has seen 111 SPAC IPOs. Based on these numbers, reporting analysts “envision the downtrend toward 100 SPAC IPOs per quarter as a bit of rationality returning to the space…expect[ing] the true steady state to be somewhere under 100 per quarter.”

Aside from the quantitative data provided in the report, mention of recent litigation issues and Securities and Exchange Commission scrutiny that SPACs are mentioned as potentially contributing to the decline.

On the other hand, de-SPAC activity has been active: 48 business combinations closed by the end of the second quarter of 2021, while 69 business combinations closed in the third quarter. PIPE transactions have played a significant role in de-SPAC and the report notes that median PIPE investments for 2021 come in at $210 million, which is an increase of over 32% from last year’s median of $158 million.

The report goes on to mention that even with 766 SPAC IPOs since the third quarter of 2020, “only 210 de-SPAC events have closed,” and, “[we’ve] still not seen a single quarter with more than 100 closed business combinations, even though SPAC IPOs have hit that mark each of the last four quarters.” Analysts find this pace to be concerning because SPACs may need to return capital to shareholders, which “would be a letdown for the SPAC structure…imply[ing] that this pathway to the public markets garnered less enthusiasm than expected from the ecosystem of private companies.”