The insurtech industry experienced some challenges in 2024, with notable shifts in funding, deal activity, and strategic investments, according to CB Insights’ State of Insurtech 2024 report. The report highlights a number of key trends shaping the industry.

Insurtech deals and funding hit lows. In 2024, deal volume continued to decline globally, from 500 deals in 2023 to 362 deals in 2024, decreasing 28% year-over-year—the lowest since 2016. This decline in deal volume outpaced the decline in the broader venture environment, which saw deal count fall 19% year-over-year. Deal funding declined from $4.7 billion in 2023 to $4.5 billion in 2024 as well. Seven mega-rounds were completed in 2024, raising $1.1 billion, with most completed during the third quarter.

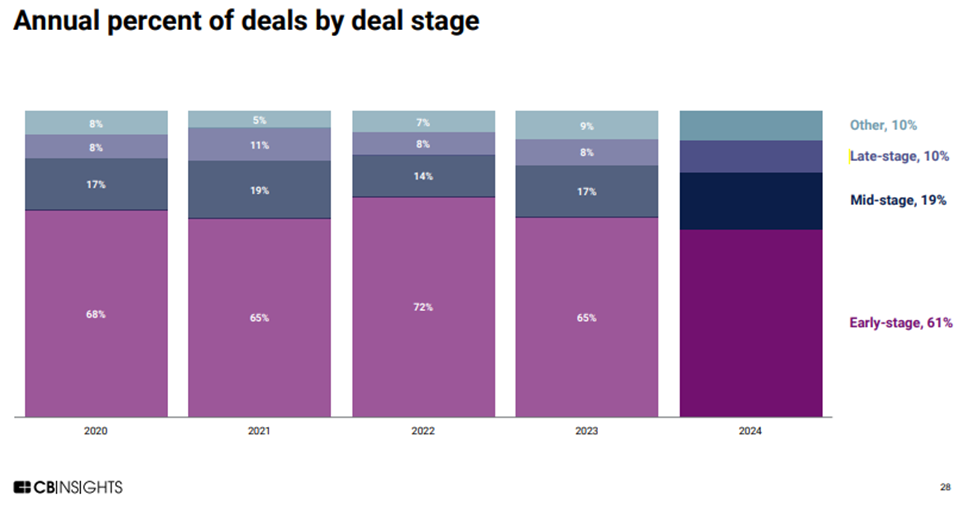

Late-stage activity. Late-stage (or Series D+) activity is up to 10% globally for all deals by deal stage, however median late-stage deal size has declined to $32.5 million in 2024 from $40 million in 2023.

Exits. The report also highlighted a decline in M&A exits, with 35 M&A exits completed in 2024. IPO activity was subdued, with only 2 IPOs completed and no insurtech companies completing de-SPAC transactions.

Geographic shift. The United States remained the dominant funding source for insurtech, with New York dethroning Silicon Valley and taking the lead in global funding for the first time since 2018. In 2024, New York’s share of global funding was 15%, more than double its 2023 share. Silicon Valley’s share of global insurtech funding dropped from 20% to just 10%.

No new unicorns. Since 2022, there have been 36 insurtech unicorns—23 in the United States, 9 in Europe, 3 in Asia, and 1 in Latin America. Seven of the ten largest unicorns are U.S.-based, with the remaining three based in Europe.

Early-stage startups stand out. Investors are placing bigger bets on fewer companies, especially in the early-stage insurtech space. The median deal size for early-stage startups increased 52% year-over-year, reaching $3.8 million in 2024. Conversely, in 2024, late-stage companies encountered challenges, with median deal sizes dropping 19% year-over-year. This decline in deal size also coincides with a restricted exit environment.

The Emergence of AI-Focused Investments. The largest deals in the P&C sector were those for AI-focused startups Altana AI and Akur8. Altana AI’s supply chain risk platform and Akur8’s pricing optimization tools demonstrate how AI is becoming a differentiator in the industry. Globally, AI funding has soared to over $100 billion, underscoring the technology’s potential to transform traditional sectors like insurance.

Access CB Insights’ report.