The Securities and Exchange Commission’s Office of the Advocate for Small Business Capital Formation issued its 2024 Annual Report just recently. The Office is required to deliver an annual report to Congress, to the Committee on Banking, Housing and Urban Affairs of the U.S. Senate and the Committee on Financial Services of the U.S. House of Representatives.

The Office was established by legislation as an independent office within the SEC to advance the interests of small business and their investors. As always, the Report provides a wealth of data on small business capital formation in the United States—extending from small and emerging companies, to later-stage businesses, to the IPO market, to smaller public companies.

Companies continue to increase their reliance on exempt offerings. In the period from July 1, 2023, to June 30, 2024, companies (excluding pooled funds) raised $949 billion in reliance on exempt offerings (including Rule 144A and Reg S offerings), compared to $28 billion in IPOs and $1.2 trillion in other SEC-registered offerings. As among exempt offering formats, not surprisingly, Rule 506(b) offerings remain quite significant with $170 billion raised in these transactions compared to only $1.5 billion in Rule 506(c) offerings. Pooled funds raised another $1.7 trillion in Rule 506(b) offerings. Offerings by pooled funds account for almost 90% of the amounts raised under Regulation D but only approximately 45% of the offerings.

The Report notes that the volume of IPOs remains down from the 2021 highs but trended up during the first half of 2024. Technology and manufacturing companies account for the largest amounts raised in IPOs. The number of VC-backed IPOs remains down quite significantly. Since 2022, IPOs by small companies have accounted for 40% of the number of IPOs but only 4% of IPO deal value.

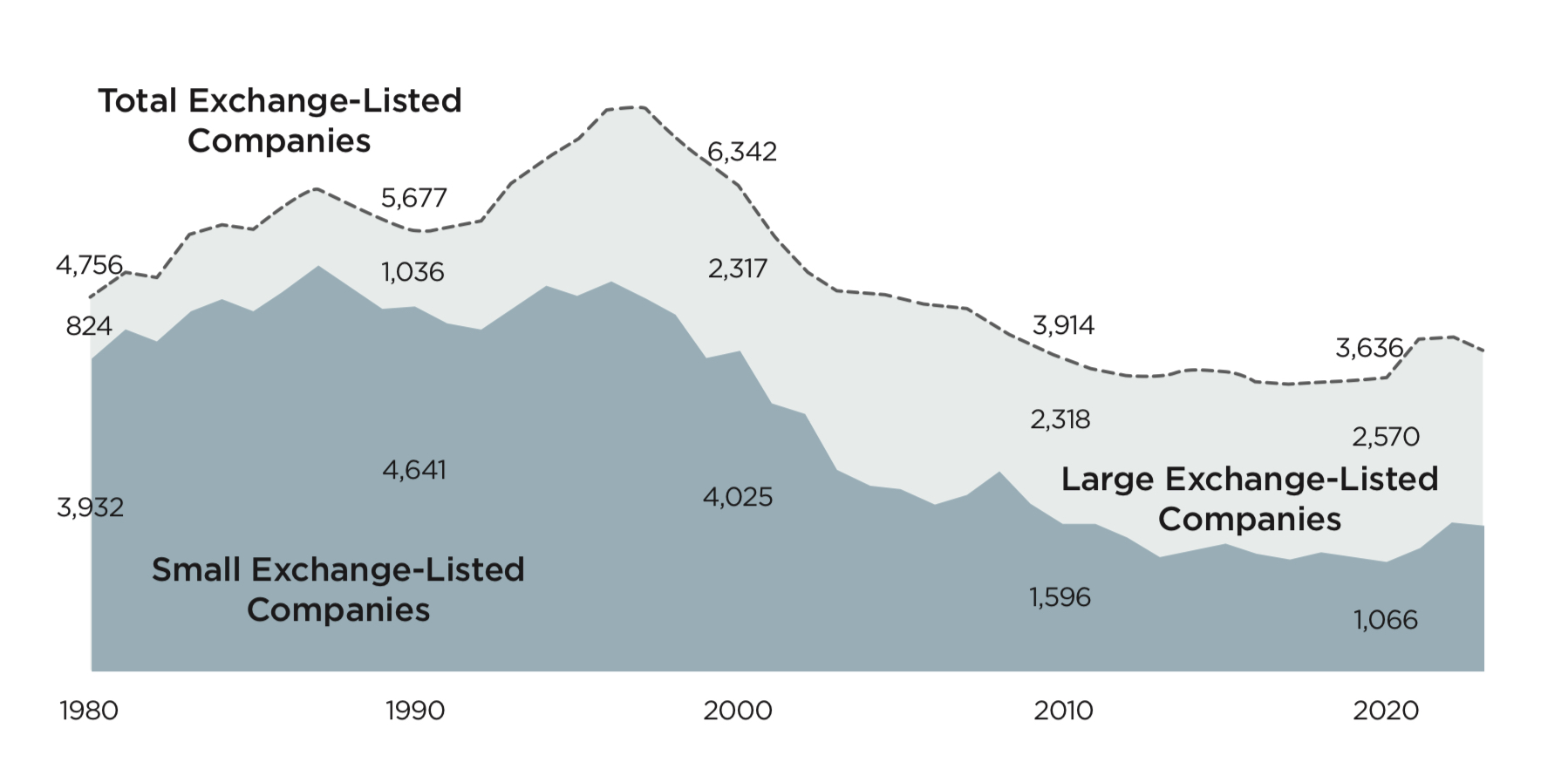

The Report provides additional insights regarding the decline in smaller public companies. For example, if one considers the overall decline in the number of U.S. public companies, the decline in the number of small exchange-listed companies is largely responsible for this trend. The Report attributes the “listing gap” to M&A activity and regulatory costs. Small public companies struggle following their IPOs. The Report notes the number of smaller companies that face issues relating to securities exchange non-compliance and that undertake reverse stock splits and that ultimately face delisting.

If ever there was a compelling basis for providing additional accommodations for smaller public companies, the analysis in the Report regarding the costs associated with being public and the impediments facing smaller public companies provides one. Perhaps a new SEC might consider this food for thought.