Since the financial crisis, the IPO market has been somewhat volatile, but in the last few quarters, the market has shown growth. A recent Audit Analytics report notes a number of factors that may contribute to the relatively slow rate of growth of the IPO market, including the abundant availability of private capital (both equity and, increasingly, debt), the overcorrection of the market for historically high IPO valuations, and M&A exits.

Based on data provided in the report, there have been 1,758 IPOs since 2008. 66% of these IPOs were completed after the enactment of the Jumpstart Our Business Start Ups (JOBS) Act. At the time of this post, there have been 27 IPOs withdrawn in 2018, according to Nasdaq. The report also notes that there has been a 46% decline in the number of SEC registrants.

Both regulators and Congress have taken steps to ease the burden of accessing the public capital markets. For example, the report highlights the expanded ability to submit draft registration statements confidentially to all companies, which took effect in July 2017. Based on Audit Analytics data, the report noted that EGCs made up 70% of all IPOs in the first quarter of 2017, and now EGCs make up almost 90% in 2018. IPO costs are one of the main reasons for companies deferring their IPOs.

Shifting focus to unicorns, Audit Analytics reported that these companies, which are valued at over $1 billion, made up only 7% of all IPOs in the first quarter of 2018. In 2017, 10 unicorns went public, which represented 2% of all IPOs completed and in 2016, 11 unicorns went public, representing 5% of all IPOs.

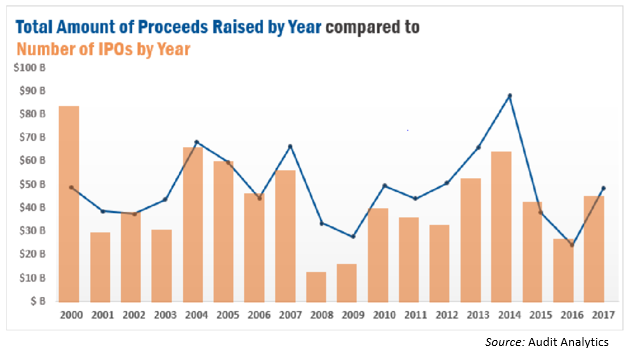

Audit Analytics also looked at total IPO proceeds raised by year, as shown above. Post JOBS Act, IPO proceeds seemed to steadily increase and then dropped again significantly in 2015 and 2016. Based on their data, the report notes that the second and third quarters are the strongest for IPO activity, which leads us to believe that 2018 will finish on a positive trajectory.

Audit Analytics also looked at total IPO proceeds raised by year, as shown above. Post JOBS Act, IPO proceeds seemed to steadily increase and then dropped again significantly in 2015 and 2016. Based on their data, the report notes that the second and third quarters are the strongest for IPO activity, which leads us to believe that 2018 will finish on a positive trajectory.

Read Audit Analytics’ full report for more.