The Securities and Exchange Commission announced an open meeting to be held on December 14, 2022 to consider a number of matters, including the final amendments to Rule 10b5-1 under the Securities Exchange Act. Late last year, the Commission proposed amendments to Rule 10b5-1 and related disclosure obligations for public companies (see our alert available here). The meeting notice is here.

Nasdaq Receives Approval for Rule Change Providing More Flexibility for Direct Listings with Capital Raise

On December 2, 2022, Nasdaq received approval from the Securities and Exchange Commission (“SEC”) to modify certain pricing limitations for companies undertaking a direct listing involving sales of the company shares in the opening auction on the first day of trading on Nasdaq.

Prior to the rule change, in order for a company to sell shares concurrent with a direct listing, the actual price must have been set at or above the lowest price and at or below the highest price of the price range established by the company in its effective registration statement. This provided less flexibility than a company has in a traditional IPO.

The rule change modifies this pricing limitation in order to provide that Nasdaq would release the security for trading if (i) the actual price is set at or above the price that is 20% below the lowest price of the disclosed price range or (ii) the actual price is set at or below the price that is 80% above the highest price of the disclosed price range. In order to rely on the extended pricing flexibility, the company is required to publicly disclose and certify to Nasdaq that the company does not expect such price would materially change the company’s previous disclosure in its effective registration statement and that its effective registration statement contains a sensitivity analysis explaining how the company’s plans would change if the actual proceeds from the offering are less than or exceed those which would be generated if the offering were to proceed at a price within the disclosed price range. Nasdaq will calculate the 20% threshold below the disclosed price range and the 80% upside limit based on the high end of the price range in the registration statement at the time of effectiveness.

As part of the rule change, Nasdaq will require that the company listing securities in connection with a direct listing with a capital raise retain an underwriter with respect to the primary sales of shares by the company and identify the underwriter in its effective registration statement. The requirement to include an underwriter likely mitigated the SEC’s concerns relating to traceability and the perceived lack of a “gatekeeper” which often arise in connection with a direct listing with a capital raise.

The New York Stock Exchange has filed a similar rule change proposal with the SEC.

The SEC’s approval can be found here.

SEC Publishes FY22-26 Strategic Plan

On November 23, 2022, the SEC released its strategic plan for fiscal years 2022 to 2026. The plan focuses on three goals: protect the investing public against fraud, manipulation, and misconduct; develop and implement a robust regulatory framework that keeps pace with evolving markets, business models and technologies; and support a skilled workforce that is diverse, equitable, and inclusive and is fully equipped to advance agency objectives.

To advance these goals, the SEC will seek to achieve a variety of objectives. It will continue to improve its capabilities to manage and analyze data to surveil the markets, promote competition and enforce the law. It will also continue to update the disclosure framework to address areas of investor demand, including, for example, issuers’ climate risks and cybersecurity hygiene policies.

Next, the SEC will address the movement of assets into private or unregulated markets and the creation of new financial products by enhancing transparency, modifying rules and developing specific regulations. To address future market volatility, the evolution in markets and rapid growth of crypto assets, it will pursue new authority from Congress, where needed, continue to collaborate with other regulators and engage more proactively on digitization initiatives.

Finally, the SEC will continue to focus on recruiting, training and retaining staff, advancing initiatives to support equal access for everyone and providing collaboration and cross-training opportunities to more employees agency-wide.

See the Press Release and the Strategic Plan.

SEC Staff Grants Temporary Relief from Compliance with Rule 15c2-11 for Rule 144A Fixed Income Securities

With the January 3, 2023, deadline fast approaching for compliance with Exchange Act Rule 15c2-11, as amended and reinterpreted by the staff of the US Securities and Exchange Commission (“SEC”) to apply to fixed income securities (the “Rule”), the SEC staff granted some temporary relief in a new no-action letter on November 30. Participants in the Rule 144A fixed-income security market, who have been grappling with how to ensure compliance with the Rule, now have an additional two years to consider the issue.

This Legal Update provides further detail, including on a petition to the SEC requesting it amend the Rule (or otherwise provide exemptive relief) to expressly exclude Rule 144A securities.

SEC Investor Advisory Committee Public Meeting Announced

The Securities and Exchange Commission’s Investor Advisory Committee announced a virtual public meeting to be held on December 8, 2022 to discuss several investor-related matters. The committee is scheduled to host three panels on the following topics: account statement disclosures; corporate tax transparency; and single stock exchange-traded funds (ETFs).

The first panel on account statement disclosures will discuss whether content and information is sufficiently conveyed to investors through account statements and account information available from firms online and through apps. The second panel is set to discuss how investors can benefit from greater corporate tax transparency. Lastly, the Committee will discuss SEC Rule 6c-11, and the risks investors may not be aware of associated with single-stock ETFs. This panel will focus on the recent rise of single-stock ETFs, ETFs that give investors leveraged returns to the daily returns of specific stocks.

The full agenda can be found here.

SEC Staff Provides Extension of Relief on Rule 15c2-11

The SEC’s Division of Trading and Markets has issued a no action letter that extends its prior relief as currently provided under “Phase 1” in its prior letter in relation to the application of Rule 15c2-11 to fixed income securities, now providing an extension until January 2025.

See the relief here. A client alert will follow.

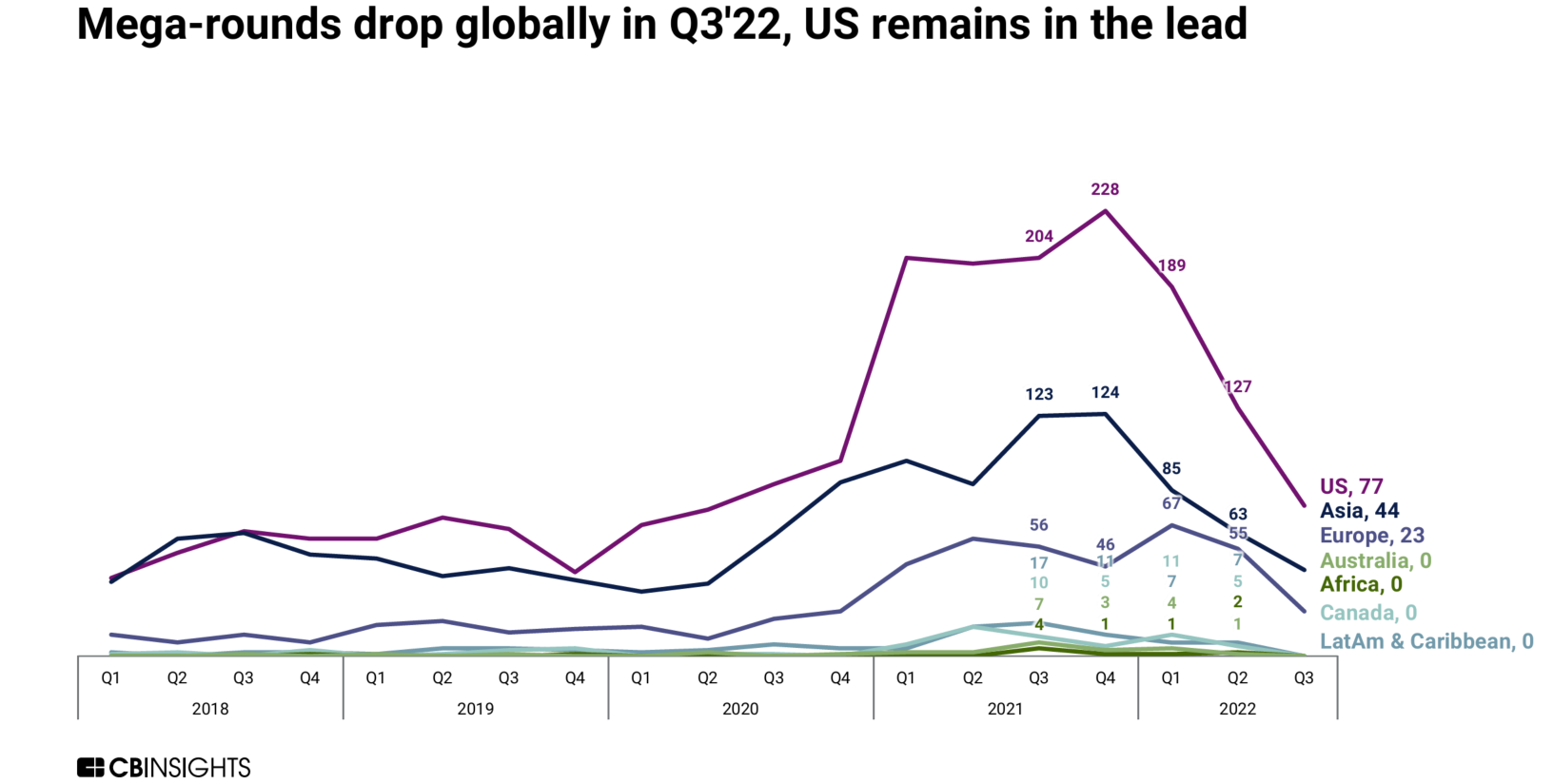

Global VC Funding Trends in 2022 Q3

The CB Insights’ State of Venture Report for the third quarter of 2022 notes that global venture funding declined to $74.5 billion in the third quarter, down 58% from the funding peak in the fourth quarter of 2021. This represents a quarter-over-quarter contraction of 34%, the largest quarterly percentage drop in a decade, with the number of deals declining by 10% to 7,936 – the lowest level since 2020. European startups experienced the largest decline in funding with 1,584 deals raising $14.8 billion in the third quarter this year, a 36% drop quarter over quarter and a seven-quarter low. The United States and Asia also saw sharp drops in quarterly funding with U.S. funding declining by 32% to $36.7 billion raised in 2,866 deals and Asia funding declining by 33% to $20.1 billion.

The number of companies that achieved unicorn status dropped across regions to 25, the lowest count since first quarter of 2020; 14 of these were in the United States. There were 144 mega-rounds completed globally in the third quarter, which accounted for $29.6 billion in funding, representing a 44% quarter-over-quarter decline and a nine-quarter low. While M&A exits continued to decline, IPOs and SPACs rebounded, with the number of SPACs reaching the highest level since 2021.

Early-stage investing constituted 66% of the overall deal share. There was a 42% drop in median deal size for late-stage rounds, indicating investors’ shrinking appetite for late-stage Series E+ deals. Asia led early-, mid-, and late-stage deal share in the last quarter. By sector, global fintech funding declined by 38% to $12.9 billion in the third quarter 2022. The retail tech and digital health sectors also saw sharp drops. In the United States, Silicon Valley startups hit an 11-quarter low with $10.7 billion raised.

EU Corporate Sustainability Reporting Directive – new sustainability disclosure obligations for EU and non-EU companies

On 10 November 2022, the EU Parliament adopted the Corporate Sustainability Reporting Directive (“CSRD”). The EU Council is expected to adopt the CSRD on 28 November 2022, after which it will be published in the Official Journal. The CSRD will then enter into force 20 days after publication and EU member states will have 18 months to integrate it into national law.

The CSRD will create new, detailed sustainability reporting requirements and will significantly expand the number of EU and non-EU companies subject to the EU sustainability reporting framework. The required disclosures will go beyond environmental and climate change reporting to include social and governance matters (for example, respect for employee and human rights, anti-corruption and bribery, corporate governance and diversity and inclusion). In addition, it will require disclosure regarding the due diligence processes implemented by a company in relation to sustainability matters and the actual and potential adverse sustainability impacts of an in-scope company’s operations and value chain.

Read the complete Legal Update.

FINRA Amends Rule 11880 to Revise the Settlement of Syndicate Accounts

On November 15, 2022, FINRA adopted amendments to revise the syndicate account settlement timeframe for offerings of corporate debt securities. The amendments to FINRA Rule 11880 establish a two-stage syndicate account settlement approach for public offerings of corporate debt securities. The amendments will become effective for public offerings of debt securities that commence on or after January 1, 2023, and will exclude any such offering that commences prior to January 1, 2023.

FINRA added a new paragraph (b)(2) to Rule 11880. The addition provides that the final settlement of syndicate accounts for any public offering of a corporate debt security must be effected by the syndicate manager by remitting to each syndicate member at least 70 percent of the gross amount due to such syndicate member within 30 days, with any final balance due remitted within 90 days following the syndicate settlement date. The amended timeframe is limited to public offerings of “corporate debt securities,” which as defined in the rule is a “debt security that is U.S. dollar-denominated and issued by a U.S. or foreign private issuer, including a ‘securitized product,’ as defined by Rule 6710(m).” For purposes of Rule 11880, a “corporate debt security” does not include a “money-market instrument” as defined in Rule 6710(o). For purposes of clarification, public offerings of convertible debt securities are not within the scope of “corporate debt security” for the amendments to Rule 11880.

See amended FINRA Rule 11880 here. See FINRA Rules 6710(m) and 6710(o) here.

Top 10 Practice Tips: Registered Direct Offerings

This practice note provides practical guidance for counsel working on a registered direct offering (“RDO”). An RDO is a public offering of securities sold on a best efforts basis by a placement agent engaged by an issuer to introduce the issuer to potential investors. An RDO is generally targeted to a select number of accredited and institutional investors, although it may be sold to non-accredited investors. Issuers find RDOs an attractive option when they are seeking to test the market or conduct an offering without attracting much market attention.

Read the complete article here.

Additional author: Kosisochukwu Ifediba